2017 State of the Industry: Soft drinks experience modest volume declines

Craft, natural sodas stave off attrition

Although carbonated soft drinks (CSDs) still is among the top performing beverage categories, more than a decade of volume declines has challenged the established category as it competes with better-for-you beverages and premium products.

“The category continues to struggle,” said Gary Hemphill, managing director of research at New York-based Beverage Marketing Corporation (BMC) in Beverage Industry’s April issue. “Volume declined for the 12th year in a row in 2016, and we believe more declines are ahead. The category has seen declines mostly in the range of 1 to 2 percent annually over the last decade. While consumers still like and enjoy carbonated soft drinks, they are increasingly opting for alternatives.”

In BMC’s August 2016 report titled “U.S. Carbonated Soft Drinks through 2020,” the market research firm anticipates that volume declines will continue. In reference to the five-year period from 2015 to 2020, it states: “In the next five years, volume is expected to decrease by 1.4 percent on a compounded annual basis. That would result in CSD volume of 11.7 billion gallons (7.8 billion cases) in 2020.”

These years of declines resulted in the category no longer being the most-consumed beverage based on volume. In BMC’s presentation “Beverages 2017: What’s in Store,” the market research firm announced that bottled water now is the most-consumed beverage by volume in the United States.

The presentation also noted that CSDs accounted for 19.8 percent of share of stomach in 2016. In comparison, the category accounted for 22.7 percent in 2011.

According to Information Resources Inc., Chicago, carbonated beverage dollar sales declined approximately one-tenth of a percent, totaling more than $27.6 billion for the 52 weeks ending May 14 in total U.S. multi-outlets and convenience stores.

In Beverage Industry’s April issue, Jordan Rost, vice president of consumer insights for New York-based Nielsen, pointed out that

88 percent of American households bought CSDs in 2016, so the category still is a competitive player in the beverage market. However, he noted consumer preferences have evolved.

“The biggest shift we’ve seen over the last decade is a redefinition of what it means to eat and drink healthfully,” Rost said. “At the same time that soda sales have steadily declined 1.1 percent over the past five years, we’ve seen a similar decline in sales of low-sugar, -salt, -calorie and -fat foods. Instead, more consumers are opting for naturally healthful products that tout organic and natural appeals and this is having a dramatic impact on soda growth dynamics.”

In its April report titled “Carbonated Soft Drinks – US,” Chicago-based Mintel explains that ongoing innovation is crucial for the established category. “In particular, suppliers will need to meet the demand for more-healthful options, varied flavors and added benefits,” the report states. “Effective engagement with iGeneration and millennials, which are increasingly ethnically diverse populations, will be central to future sales growth.”

Although the CSD market is facing its share of challenges, the category still had pockets of growth that helped stave off some of the attrition.

“Despite overall category declines, sales of ginger ale actually grew 9 percent in 2016,” Nielsen’s Rost said in Beverage Industry’s April issue. “More consumers focused on gut health are likely opting for the functional and digestive health benefits of ginger-based soda. While many consumers clearly still want to indulge in soft drinks, they’re turning to ginger ale as a way to still impart some health benefits.”

He added: “In spite of overall category decline, sales of natural soft drinks are growing at 16 percent annually. However, these natural varieties still account for less than 1 percent of total soft drink sales, so natural sodas are a long way away from reaching significant scale. On the other hand, sparkling waters are now purchased by more than one in three American households. I would expect soft drink manufacturers to look outside the CSD category and blur the lines between what we’ve traditionally known as soda.” BI

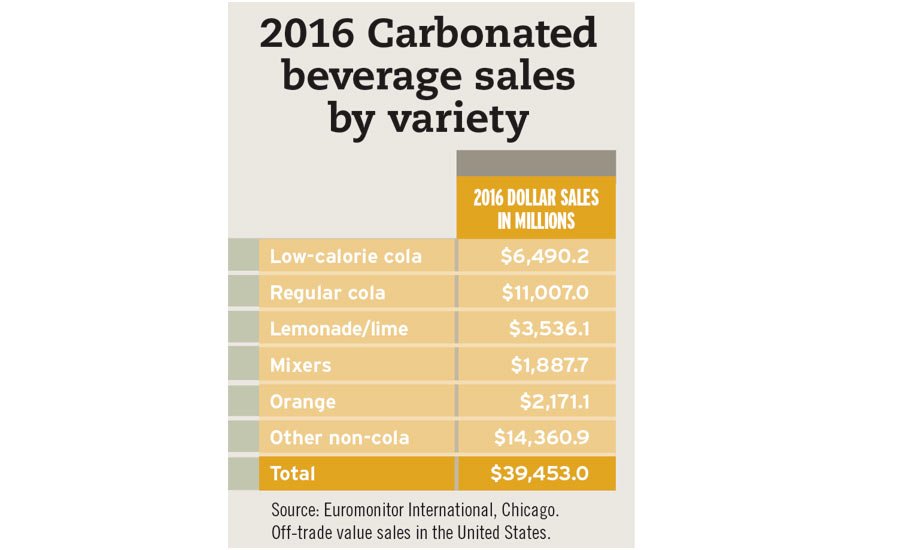

Carbonated beverage sales by variety

(Individual brands)

| Low-calorie cola | $6,490.2 |

| Regular cola | $11,007.0 |

| Lemonade/lime | $3,536.1 |

| Mixers | $1,887.7 |

| Orange | $2,171.1 |

| Other non-cola | $14,360.9 |

| Total | $39,453.0 |

*Includes brands not listed.

Source: Information Resources Inc. (IRI), Chicago. Total U.S. supermarkets, drug stores, gas and convenience stores, mass merchandisers, military commissaries, and select club and dollar retail chains for the 52 weeks ending May 14.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!