Alternative capital solutions can offer reprieve to manufacturing sector

Sale leaseback can help beverage manufacturers raise capital while navigating tariffs

American manufacturers are about to be handed a very large bill. Wherever this administration’s tariffs ultimately settle, with imports in the trillions, the tab for tariffs is going to be in the billions. Tariffs will not only impact the bottom line of American manufacturing companies, but derivatively, also impacting how manufacturers think about their enterprise as a whole.

As beverage manufacturers find themselves considering a variety of financing alternatives while navigating the new landscape, a sale leaseback might be among the most attractive options.

Good for manufacturers

As if there weren’t good reasons already for American manufacturers to have access to more capital, the likelihood of tariffs impacting cash flows creates another reason. All conventional sources of capital — term loans, lines of credit, bond sales — should continue to be considered when there is a pending capital need.

Another source that is highly strategic for manufacturers in today’s political and economic environment, yet not quite part of the standard capital alternatives playbook, is the sale leaseback. As the name implies, the sale leaseback transaction involves selling company-owned real estate, then leasing it back under a long-term lease.

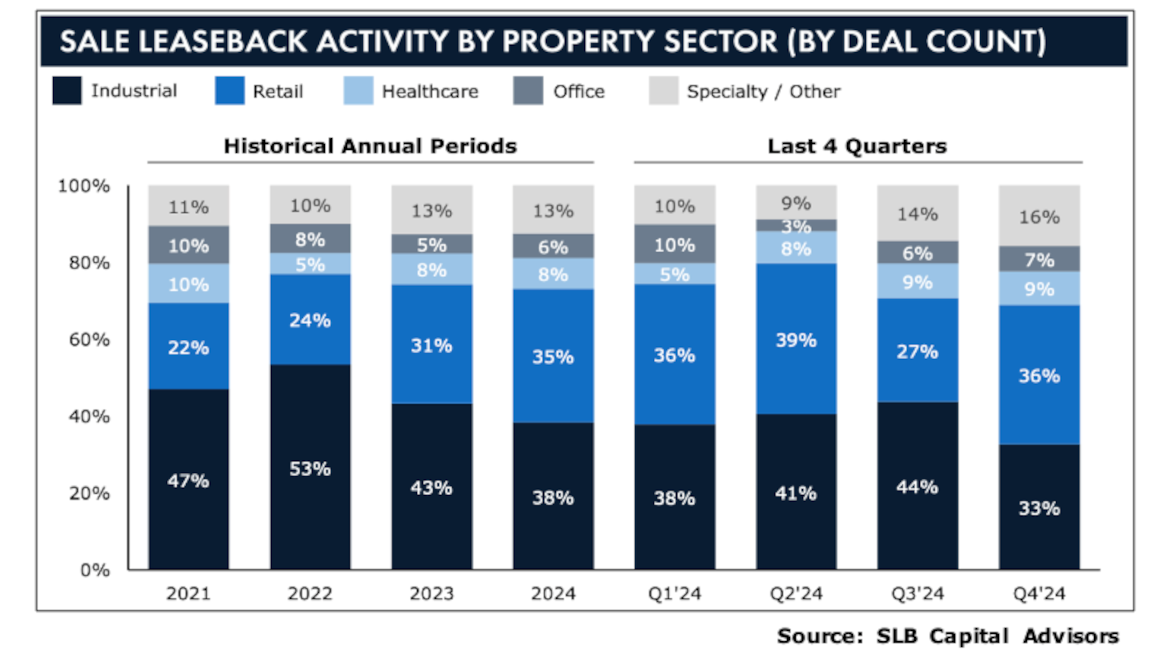

Raising capital from sale leasebacks is particularly apt for manufacturers for two reasons. First, many manufacturers own their facilities and second, industrial real estate is in high demand among investors in the United States. In 2024, industrial transactions made up 38% of all sale leaseback deals.

Making the case

Underlying real estate even in non-core locations typically enjoys a premium valuation as compared with standard manufacturing companies, which often have an enterprise value based on mid-to-high single-digit EBITDA multiples.

This dynamic enables the sale leaseback to unlock value sitting quietly on the balance sheet. As a result, not only can sale leaseback transactions offer manufacturers a multiple arbitrage but proceeds from a sale leaseback can be utilized for growth, pending tariff payments, or funding acquisitions, among a range of uses.

A case in point

Sale leasebacks can be used by large and small companies. In addition, they are agnostic ― regardless of what a company is manufacturing, it can reasonably consider a sale leaseback. The following are some recent transactions:

Early this year, Aztalan Engineering, a contract manufacturer in Lake Mills, Wis., sold and leased back its headquarters. The firm raised $5.1 million in the sale leaseback deal, allowing them to fund acquisitions of other companies.

In December, DBG Arkansas LLC, a manufacturer of metal products for the automotive, heavy truck and appliance industries, raised $15.7 million in a sale leaseback deal involving its 642,000-square-foot industrial facility in Conway, Ark.

In September, Douglas Dynamics, manufacturer and up-fitter of commercial work truck attachments and equipment, raised $64.2 million selling facilities in five locations then leased the properties back from the buyer TPG Angelo Gordon. Douglas Dynamics' Executive Vice President and Chief Financial Officer said the deal will enable the company to “Optimize our balance sheet and better position ourselves for future investments in the business.”

Also in September, Incodema3D, a leader in direct metal 3D printing for aerospace and automotive industries, raised millions by selling its state-of-the-art manufacturing facility in Freeville, N.Y., and leasing it back from buyer ME Commercial.

In August, Univar Solutions, a global specialty chemical and ingredient distributor, raised more than $60 million through a sale leaseback transaction with Fortress Net Lease.

Sticking points

Some C-suite executives are concerned about selling mission-critical real estate assets. These fears are misplaced and can be allayed by how the sale leaseback agreement with the buyer is negotiated. Lease terms are typically 15-20 years, with options for another 20 years or more. Ultimately, the seller can maintain effective control of the property for well past 40 years.

Additionally, sale leaseback investors are credit investors first. A solid financial profile will drive the optimal outcome, since buyers are underwriting the credit of the tenant.

Another common concern for business owners is that a planned change of control, i.e., selling the business in whole or in part, might be impeded by a long-term lease obligation. This is a legitimate concern that can be addressed and successfully mitigated through thoughtful negotiations of the long-term lease itself in the sale leaseback transaction.

Finally, many chief executives might balk at the complexity of a sale leaseback transaction and selling off a key asset, when a plain vanilla mortgage could accomplish the objective of raising capital. However, a mortgage enables a borrower to tap less than the full value of their real estate holding while a sale leaseback transaction enables an owner to extract full value.

For example, a $10 million real property would illustratively allow a manufacturer to borrow perhaps $7-8 million against it. By contrast, a sale leaseback transaction will enable the manufacturer to access 100% of the building’s value, or the full $10 million.

Manufacturing is difficult. Shifting technology, finding and retaining labor, intense competition, and fickle end markets all add to the degree of difficulty. Add to this list navigating tariffs and managing the fallout of raising prices to cover a new layer of costs. All sources of capital should be considered by manufacturers and for the manufacturers that own their real estate, a nuanced source of capital, the sale leaseback, is worth consideration.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!